The Daily Digital Wallet and the Transformation of Small Transactions

April 10, 2026

Key Highlights:

● Mobile payments are transforming how consumers handle everyday small transactions.

● Digital wallets streamline payments, making cash and cards less necessary.

● The rise of fintech solutions is driving greater adoption of mobile payment apps.

● Retailers benefit from faster transactions and better consumer insights.

● Security and convenience are the primary motivators for consumers shifting to digital wallets.

Estimated Reading Time: 12 minutes ┃Post by Jordan Mercer

In the past decade, the way consumers manage small transactions has undergone a profound transformation. From buying a morning coffee to paying for public transit, digital wallets have reshaped the experience of everyday payments. Mobile payment platforms such as Apple Pay, Google Wallet, and emerging fintech solutions have not only simplified the process but also begun to influence broader economic behaviors, prompting both consumers and merchants to rethink how money flows in the digital age.

The Rise of Mobile Payments

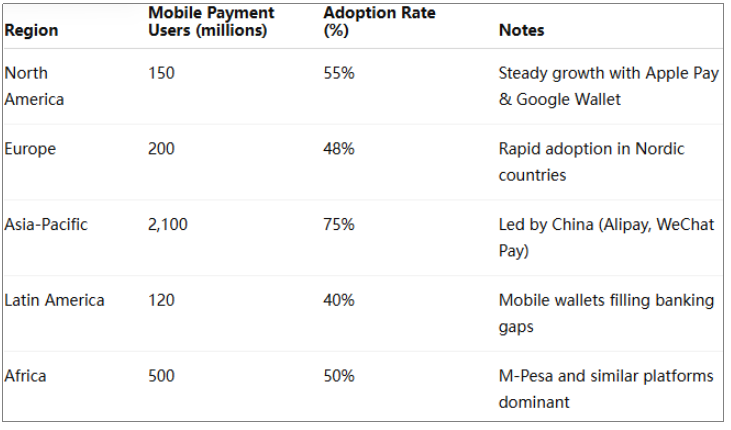

Digital wallets offer users the ability to store credit and debit card information securely on their mobile devices. This capability allows payments to be executed quickly through near-field communication (NFC), QR codes, or app-based transfers. According to recent studies, the number of mobile payment users worldwide is projected to surpass 3 billion by 2026, reflecting a significant shift in consumer habits from traditional payment methods.

(Table 1- Mobile Payment Adoption by Region (2026 Projection))

Several factors drive this growth. First, convenience is a major motivator. Consumers no longer need to carry cash or multiple cards for minor purchases. Second, mobile payments are increasingly integrated into apps and services that consumers use daily, such as ride-hailing, food delivery, and retail loyalty programs. This integration creates an ecosystem where spending, rewards, and financial management converge seamlessly.

How Small Transactions Are Changing

Small transactions, often referred to as microtransactions, were historically cumbersome due to the logistical constraints of handling coins and cash. Mobile payments have removed much of this friction. A coffee, a bus fare, or a quick snack can now be paid in a matter of seconds. This ease of transaction encourages consumer spending on smaller items, creating a subtle but meaningful effect on the overall economy.

For merchants, the shift is equally impactful. Retailers benefit from faster checkouts, reduced cash handling, and enhanced data collection. Each mobile transaction provides valuable insights into consumer behavior, from purchase frequency to preferred payment methods, allowing businesses to optimize pricing strategies, stock management, and targeted promotions.

Financial Inclusion and Accessibility

Beyond convenience, mobile payments also promote financial inclusion. In regions where banking infrastructure is limited, digital wallets provide access to financial services without the need for traditional bank accounts. For example, in parts of Africa and Southeast Asia, mobile payment systems like M-Pesa have become critical to everyday commerce, enabling users to send, receive, and store money via mobile phones. This democratization of financial services has profound economic implications, facilitating participation in both local and global markets.

Security and Consumer Trust

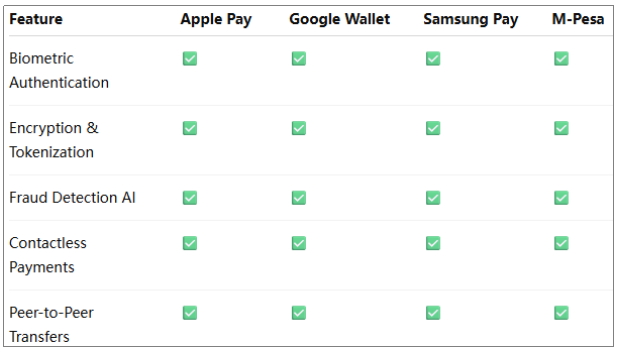

Security remains a top concern for mobile payment users. Digital wallets employ encryption, tokenization, and biometric authentication to safeguard transactions. While these technologies significantly reduce the risk of fraud compared to cash or physical cards, consumer trust is essential for adoption. Financial literacy initiatives and clear communication from fintech providers are critical in reassuring users about data privacy and transaction safety.

(Table 2- Security Features of Popular Digital Wallets)

Interestingly, research suggests that the perception of security directly correlates with mobile payment adoption. Consumers who feel confident in their device’s security are more likely to use digital wallets for both minor and larger purchases. Consequently, fintech companies are investing heavily in advanced fraud detection systems, AI-driven anomaly monitoring, and customer education to foster trust.

Economic Implications

The widespread adoption of mobile payments has broader economic implications. Small businesses, in particular, benefit from quicker cash flow and lower transaction costs. Micro-merchants and gig economy workers, who may operate on thin margins, find mobile payments an essential tool for operational efficiency.

Moreover, the cumulative effect of millions of microtransactions contributes to national and regional economic activity. Governments and central banks are increasingly exploring digital payment infrastructures to complement traditional monetary policy tools, recognizing that mobile payments generate real-time data on spending trends and economic health.

The Future of Everyday Transactions

Looking ahead, the digital wallet ecosystem is poised to expand further. Innovations such as cryptocurrency integration, cross-border payment solutions, and AI-driven financial management tools are set to redefine small transactions. As more devices—smartwatches, voice assistants, and even connected vehicles—become capable of executing payments, the frictionless exchange of value will become an intrinsic part of daily life.

Yet, challenges remain. Ensuring cybersecurity, maintaining interoperability among payment platforms, and addressing privacy concerns are critical to sustaining growth. Policymakers, fintech innovators, and consumers must collaborate to create an inclusive, secure, and efficient digital payment ecosystem.

In conclusion, mobile payments are not just a convenience—they are reshaping the fabric of everyday commerce. The daily digital wallet is becoming as indispensable as the smartphone itself, transforming how people spend, save, and interact with the economy on a micro scale. As this trend continues, both individuals and businesses stand to gain from a faster, safer, and more connected financial experience.

(The content in this article is intended for informational purposes only and should not be considered financial advice. Readers should conduct their own research and consult financial professionals before making decisions related to digital payments or fintech solutions.)

FAQs:

1. Are mobile payments safe for all types of

purchases?

Yes, digital wallets employ strong encryption and authentication measures,

but users should remain vigilant and use devices with updated security features.

2. Can mobile

payments replace cash entirely?

While adoption is growing rapidly, cash remains

essential in some regions and scenarios. Mobile payments are likely to complement rather than

fully replace cash.

3. Do mobile payments

incur fees for small transactions?

Most consumer-facing wallets do not charge fees

for everyday purchases, but merchants may experience nominal transaction fees depending on the

platform.

About Author

Jordan Mercer is a fintech analyst and economic commentator with over a decade of experience exploring digital payments, financial inclusion, and the evolving landscape of consumer finance. Jordan has contributed to industry reports and policy recommendations on mobile payment adoption and emerging financial technologies.

References

[1] World Bank.

(2023). Digital financial services and inclusion.

[2] Statista. (2026). Number of mobile payment users worldwide from 2018 to 2026.

[3] McKinsey & Company. (2022). The future of payments: How digital wallets are transforming commerce.

Explore more insights on this blog to stay informed about the latest trends shaping the global economy!