How Everyday Habits Add Up to Big Expenses?

April 8, 2026

Key Takeaways:

● Everyday spending adds up in ways most people don’t fully realize.

● Small, routine purchases like coffee and snacks have a measurable long-term economic impact.

● Commuting costs are a significant, often overlooked component of monthly expenses.

● Tracking daily expenditures provides insights for better budgeting and financial planning.

Estimated Reading Time: 8 minutes ┃Post by Clara Bennett

The costs of daily living often feel invisible. We swipe cards, tap phones, or even carry cash without noticing how small purchases accumulate over weeks, months, and years. While large expenses like rent, utilities, and insurance dominate financial discussions, the subtler costs of everyday life—coffee, lunch, rideshares, and commuter fuel—can quietly erode savings and affect long-term financial health. Understanding these hidden expenditures is not merely an exercise in bookkeeping; it is essential for personal economic empowerment.

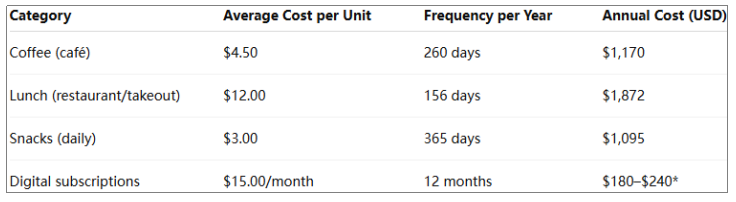

For millions, the day begins with coffee. According to a 2023 survey by the National Coffee Association, approximately 62% of Americans drink coffee daily. The average cost of a regular coffee from a café hovers around $4.50. At first glance, this seems manageable. However, let’s calculate the cumulative impact: five days a week over 52 weeks equals 260 coffee purchases annually, totaling $1,170. Add a flavored latte or occasional splurge, and this figure can easily exceed $1,500 per year. For households aiming to maximize savings or invest in long-term goals, understanding this pattern is vital.

*Varies depending on number of subscriptions.

(Table 1: Annual Costs of Common Daily Expenses)

Beyond the financial aspect, coffee spending often reflects broader lifestyle habits. Many consumers opt for convenience over cost-efficiency, choosing premium cafés or on-demand delivery instead of brewing at home. While this decision can enhance daily convenience, it also highlights the importance of evaluating personal priorities against economic realities.

The Daily Commute: More Than Gasoline

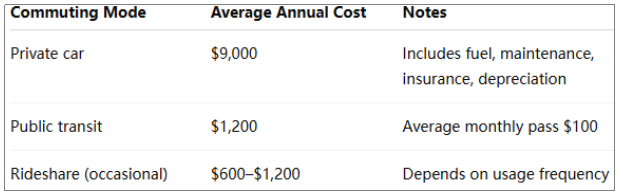

Another significant hidden cost is commuting. Whether driving, riding public transportation, or using rideshare services, daily transit can consume a considerable portion of income. For example, the American Automobile Association (AAA) estimates that the average cost of owning and operating a vehicle exceeds $9,000 per year, accounting for fuel, maintenance, insurance, and depreciation.

(Table 2- Commuting Costs Comparison)

Even public transit is not immune from cumulative expenses. A monthly metro or bus pass averaging $100 may appear modest, but over a year, it sums to $1,200, excluding occasional taxis or ride-hailing services. Combining these commuting costs with other daily spending patterns illustrates the total economic footprint of routine life—an amount that can rival larger, more obvious expenses when aggregated over time.

Meals, Snacks, and the Convenience Premium

Lunch breaks, snack runs, and spontaneous takeout are further contributors to everyday financial strain. A typical $12 lunch purchased three times a week totals $36 weekly or $1,872 annually. Snack purchases, often small but frequent, may cost `$1-5 daily, translating to an additional `$1-1,200 per year.

Convenience carries a premium, and the pattern is widespread. Consumers frequently overvalue immediate satisfaction or time savings while underestimating cumulative cost. The subtle yet substantial impact of these choices reinforces the value of financial literacy and conscious spending.

Subscription Services and Small-Scale Digital Spending

In addition to tangible items, digital subscriptions—streaming services, apps, and premium content—represent a modern, often overlooked expense. The average American subscribes to five or more digital services, averaging `$1-20 per month each. Annually, this can amount to `$1-1,200, comparable to or exceeding other day-to-day costs.

While individually these services seem affordable, collectively they reflect a broader trend: recurring micro-payments can silently divert resources that might otherwise fund investment or emergency savings. Awareness of these commitments is crucial in shaping a financially resilient lifestyle.

The Long-Term Financial Impact

The accumulation of small daily costs may appear trivial in isolation, but over time, they form a significant financial burden. A household spending $10 daily on coffee, snacks, and lunch spends $3,650 annually—a figure large enough to fund a partial vacation, emergency fund, or retirement contribution.

Recognizing these patterns enables strategic planning. By substituting certain expenditures—brewing coffee at home, preparing lunches, or limiting occasional premium purchases—households can redirect resources toward long-term financial objectives. Even modest reductions in daily spending can compound over years, creating meaningful financial security.

Tracking and Analysis: Tools and Methods

Modern technology offers tools to track and analyze everyday spending effectively. Apps like Mint, YNAB (You Need a Budget), and personal finance spreadsheets provide detailed insights into spending habits. Categorizing expenses—commuting, meals, subscriptions, entertainment—allows users to visualize where money flows and identify potential savings.

Regular financial audits, even brief monthly reviews, can reveal surprising trends. Many individuals overestimate discretionary spending or underestimate recurring costs. By systematically tracking expenditures, consumers gain actionable insights that foster informed decision-making and behavioral adjustments.

Behavioral Economics and Everyday Spending

Behavioral economics illuminates why people underestimate small expenses. Concepts like “mental accounting" and “present bias" explain how individuals prioritize immediate gratification over future financial benefits. Recognizing these tendencies encourages the adoption of strategies to mitigate impulsive spending.

For instance, pre-committing to home-brewed coffee or meal prepping for the week reduces exposure to convenience-driven expenditures. Similarly, bundling subscriptions or setting automated savings transfers can counteract the subtle drain of recurring micro-payments. Small behavioral changes can thus have an outsized impact on overall financial well-being.

Planning for Financial Resilience

Understanding the real cost of everyday life extends beyond budgeting; it informs broader financial resilience strategies. By identifying discretionary spending and cumulative small expenses, individuals can allocate funds for investments, emergency savings, and retirement accounts.

Moreover, awareness of lifestyle costs can guide career decisions, housing choices, and long-term planning. For example, choosing a residence closer to work may reduce commuting expenses, while investing in energy-efficient home solutions can lower utility bills. Each decision, informed by a detailed understanding of everyday spending, strengthens overall economic stability.

From the first

sip of coffee to the daily commute, the hidden costs of everyday life accumulate faster than

most realize. By carefully tracking expenditures, analyzing patterns, and implementing small

adjustments, individuals can achieve meaningful savings and financial security. These

insights highlight the importance of conscious spending, strategic planning, and the value

of financial literacy in navigating modern life.

(The content of this article is intended for

informational and educational purposes only. It does not constitute financial

advice, investment guidance, or recommendations. Readers should consult

qualified financial professionals for personalized

advice.)

FAQs:

1. How can I

start tracking my daily expenses effectively?

Start with a simple spreadsheet or a

budgeting app, categorize your expenses, and review weekly for patterns.

2. Are small

purchases really that impactful?

Yes. Even minor daily expenses accumulate

over time, often exceeding hundreds or thousands of dollars annually.

3. What

strategies can reduce everyday spending without feeling

deprived?

Meal prepping, home-brewing beverages, consolidating subscriptions,

and prioritizing value over convenience are effective approaches.

About Author

Clara Bennett is an economist and personal finance writer with over 12 years of experience analyzing household spending patterns. She specializes in translating complex economic concepts into practical advice for everyday financial decision-making. Her work has appeared in several industry journals, and she frequently consults on personal finance education initiatives.

References

[1]

National Coffee Association. (2023). National Coffee Drinking Trends.

[2] American Automobile Association. (2022). Your Driving Costs.

Stay tuned and explore more insightful content on this blog to master the economics of everyday life!